Two Weeks in Review (W21-W22): The Baseline for How We Read AI Adoption

This is the first two-weeks-in-review for The Hype Check and the baseline for our method. We score news against customer-facing levers, then separate signal from announcement noise.

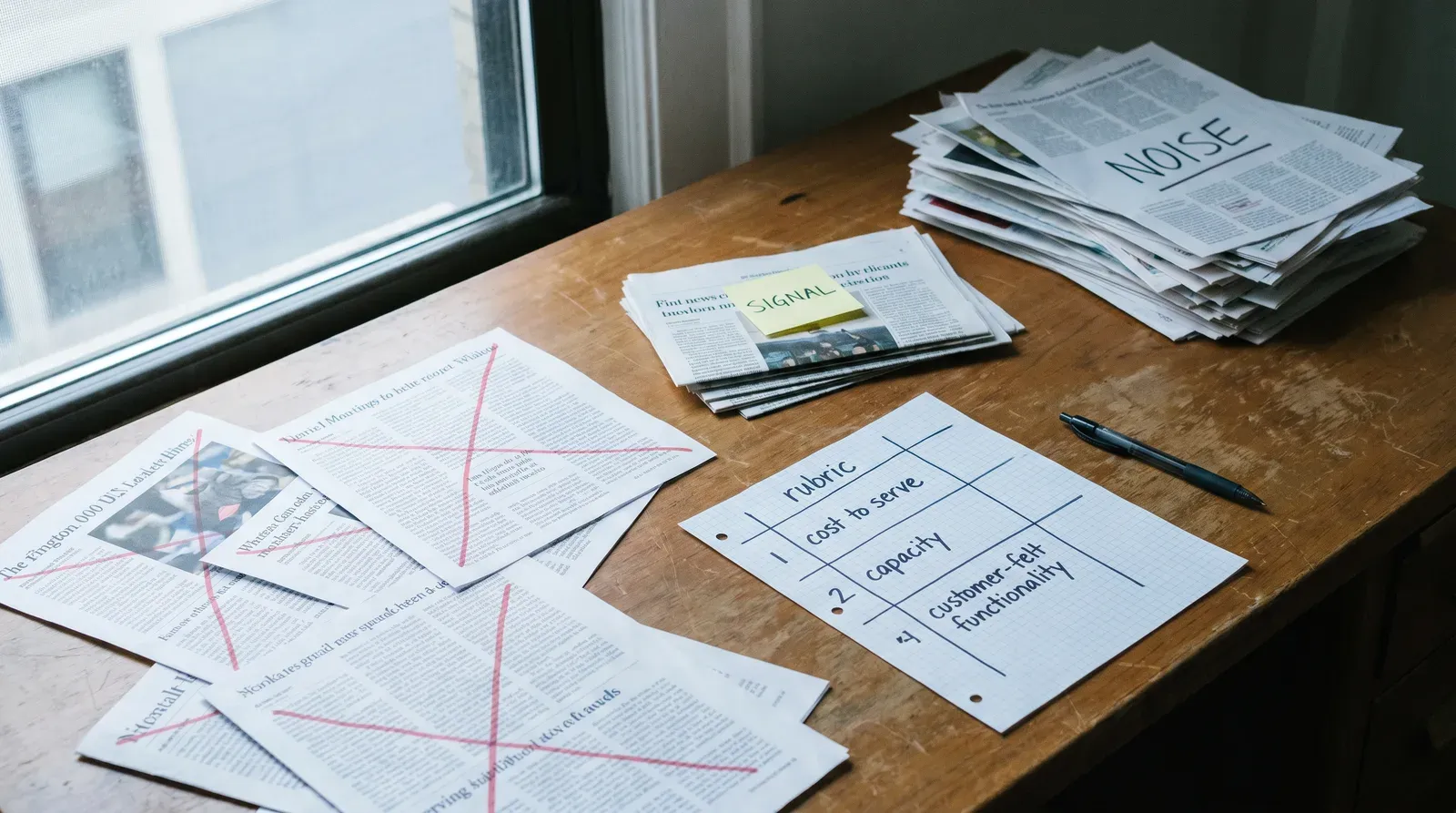

Most AI weekly recaps are doing distribution work for vendor PR. They track launches, model names, funding headlines, conference moments, and partnership announcements. Then they call that market intelligence.

That is not useful enough for leaders carrying service quality, margin, and execution risk at the same time. A recap that cannot tell you what changed for customers is noise with better formatting.

Our standard is stricter and easier to audit. Every two weeks we score the window against one question: did anything in this period move a real customer-facing lever, same service at lower cost-to-serve, the same team serving more customers, or product functionality the customer actually feels?

Everything else is context we note, then walk past.

This baseline edition does one thing publicly: it applies that standard to W21 and W22, May 17 to May 30, so readers can see the filter, disagree with it, and test whether our calls hold up over time.

Most “AI weekly recaps” amplify vendor announcements and call it analysis. We do the opposite. Every two weeks we score the news against one question: did anything published in this window move a real customer-facing lever, same service at lower cost-to-serve, the same team serving more customers, or product functionality the customer actually feels? Everything else is noise we have to walk past to find the signal.

What Was In the Air (W21-W22)

The window was crowded with workforce-scale vendor deployment stories, capital and model stack signaling, and enterprise enablement claims: KPMG and Anthropic announcing broad rollout coverage at 276,000 people on May 19 with Bill Thomas and Rema Serafi on record, Anthropic launching Opus 4.8 on May 28 with stronger capability claims and a public cost note from Databricks CTO Hanlin Tang that token cost was “61% cheaper” than Opus 4.7, and PwC extending AI training to 30,000 professionals from its May 14 release with Paul Griggs and Advocate Health’s Andy Crowder on record. Around that, pressure from EU AI Act enforcement kept rising, DeepSeek remained a live capability topic after the craze phase but with thin named enterprise deployment evidence in the last 60 days, and the acceptance-adoption gap stayed visible: many organizations sounding committed while real operating change lagged.

The Three-Lever Filter, Applied

Cost-to-serve

The most plausible cost-to-serve signal in this window came from the model economics conversation around Opus 4.8. If a leading enterprise platform CTO publicly says the new model runs at materially lower token cost than the prior version, that can matter, but only as a potential. Lower model unit cost is not the same as lower service cost unless workflow design, guardrail overhead, retry rates, and human review burden also move in the right direction. The claim is meaningful as input to an efficiency hypothesis, not as proof that customers are now cheaper to serve.

KPMG’s May 19 workforce-scale announcement can also indicate cost pressure being taken seriously, because organizations do not stage rollout language at that size unless they expect operating leverage. But this surface is still vendor-curated. Public statements by Bill Thomas and Rema Serafi tell us intent, partnership scope, and ambition. They do not yet give enough independent evidence that a customer-facing service line is delivering the same or better outcome with lower cost-to-serve in production.

What looked like cost movement but did not clear our bar? Broad “enterprise AI acceleration” framing without a named buyer metric, a before-and-after service baseline, or a specific process where total cost dropped. DeepSeek discussion is similar in this window: capability is real, but recent named enterprise deployment evidence is too thin to conclude cost-to-serve movement at customer edge.

Capacity to serve more

This is where workforce-scale moves can become signal fastest, if we see proof of throughput. PwC’s 30,000-professional training program is important because large-scale enablement can convert into more customers served without linear headcount growth. The public record through Paul Griggs and Andy Crowder gives us directional credibility: this is not a lab-only story and includes a practical service context.

Still, this is not yet definitive capacity evidence. Training completion and platform access are upstream indicators. They are not the same as cycle-time reduction, queue shrinkage, first-contact resolution improvement, or higher customer volume handled at maintained quality.

The KPMG-Anthropic announcement also sits in this same middle zone. Workforce scope at 276,000 suggests potential for expanded serving capacity, but the window did not provide named buyer evidence showing that a specific customer-facing process now handles more demand with the same team and quality controls. In our lens, that keeps it in plausible, not proven.

What looked like capacity movement but did not clear? Generalized language about “AI-ready workforce” and “enterprise-wide transformation” without transparent operational deltas. The market still often treats preparedness as adoption and adoption as throughput. Those are different steps.

Functionality customers feel

The strongest possible signal under this lever is simple: the customer can now do something they could not do before, or can do it materially better, and that difference is observable outside internal demos.

In this two-week window, model-side progress around Opus 4.8 may enable better customer-visible experiences, especially where reliability and reasoning quality have been blocking full rollout. That is a plausible pathway. It is not yet customer-experienced evidence by itself. A model release, even with credible cost commentary, remains supplier-side until we see named buyer outcomes in live workflows.

DeepSeek sits at the same boundary from the opposite direction. The market attention was intense, and capability arguments remain serious. But in the last 60 days of this window, named enterprise deployment evidence tied to customer-felt functionality has been thin. Without that, the story stays in watchlist status for this lever.

What looked like customer-felt movement but did not clear? Feature claims presented only through vendor channels with no independent buyer voice on adoption depth, quality impact, or sustained usage. When the evidence surface is curated by suppliers, we label it as such and hold judgment.

The Honest Miss

This lens under-counts two things that matter. First, regulatory pressure, especially around EU AI Act enforcement, can force operating changes before any of the three customer levers move cleanly in published data. Second, trust and voluntariness in agentic rollouts affect long-term adoption quality, even when short-term cost or throughput metrics look strong. Those dimensions do not map neatly to cost-to-serve, capacity, or customer-felt functionality. We are keeping the three-lever frame as the core because it is auditable, and we will test where it fails in future editions instead of pretending it is complete.

What Earns Coverage Next

- A named buyer voice from the last 60 days that is not vendor-curated.

- A plausible, testable link to at least one of the three levers.

- Something AIRS or our own investigation can add that the announcement itself cannot.

The Standing Offer

Every two weeks, on Sunday, we will publish this review. It is a slow read in a fast medium on purpose. If this lens calls a story wrong, we will say that in the next edition and update the rule in public. If you disagree with this baseline, send the strongest counterexample you have. The point is not to protect a framework. The point is to improve decision quality for people who have to run real customer operations.